After declining in first quarter, market recovers in following quarter, with expected 2013 revenue of $2.2 billion.

After declining in first quarter, market recovers in following quarter, with expected 2013 revenue of $2.2 billion.

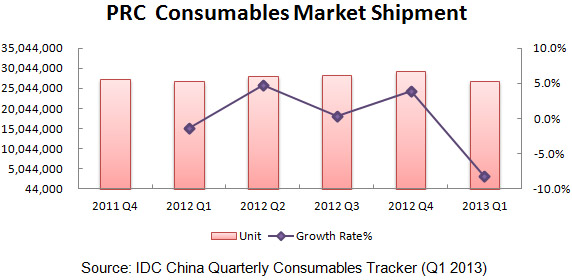

IDC’s China Quarterly Consumables Tracker showed that the total shipment of printing consumables in China during the first quarter of 2013 declined 8.2 percent compared to the previous quarter at 29.96 million units, with revenue falling six percent to $530 million (€400.4 million).

However, Raymond Huo, Senior Market Analyst, Computing Systems Research at IDC China said that due to “steady growth in printer sales and recovering market demand, IDC forecasts that 2Q13 will see a significant rebound in both the shipment and the revenue of printing consumables”, adding that the annual revenue “is expected to grow by 12.7 percent over last year, while the total revenue of inkjet and laser consumables will amount to $2.2 billion (€1.6 billion)”.

Huo explained that the first quarter of a year “is usually a low season for the sales of printing consumables”.

The IDC tracker also found that, while cartridges always dominate the inkjet consumables market, continuous ink supply systems (CISS) are gradually eroding the market share, with many CISS brands gaining good reputations among SME customers due to being more economical and practical.

A further finding was that more compatible vendors are opting out of the cartridge-dominated inkjet consumables market in favour of the wider commercial laser consumables market due to the increasing costs of recycling, processing and re-engineering products, as well as the technical improvement of DIY products and the impact of CISS. As a result, shipment of inkjet consumables in 1Q13 reduced by 3.9 percent compared to the same quarter in 2012, while laser consumables shipment increased by 7.8 percent.

IDC discussed the competition between original cartridge vendors and increasingly growing compatible brands in the laser consumables market, noting that the implementation of government procurement and subcontract policies has helped the compatible brands with huge price advantage to obtain wider market room, causing OEMs to lose some industrial customers, with over 80 percent of the market dominated by compatible brands. It added that OEMs “need to attach more importance to retaining the existing customers and enlarging the market demand from emerging industries”.

In terms of counterfeit products, IDC noted that they have been following along with market development, although anti-counterfeiting activities and technical upgrades by OEMs have significantly restrained the counterfeit sales channels. However, the firm said that the “explosive growth” in size of the internet sales market has meant that network has increasingly become the main channel for counterfeit product sales, and so they continue to be a threat.