The latest information from IDC suggests slower declines in units and shipment values in 2Q13.

The analyst reported that “after several quarters of notable decline”, the global market for hardcopy peripherals has begun to show “encouraging signs of recovery”, with its smallest year-over-year decline in shipments of -1.8 percent, the lowest since 4Q11. 26.1 million units were shipped in 2Q13, suggesting a “relatively stable hardware market”, and the value of the market, at $13.8 billion (€10.3 billion), declined only -1.7 percent year-over-year.

IDC added in turn that this previous quarter is the first since the final quarter of 2010 where the US and Western European markets saw positive year-on-year growth in unit shipments, of 1.4 and 3.9 percent respectively. IDC previously reported the positive results for the Western European market, as The Recycler discussed earlier this month.

Despite the decline, IDC noted it is “optimistic” about growth opportunities in the global market, adding that high speed monochrome segments (from 31 to 44 and 45 to 69ppm), along with colour laser, are driving “the best growth prospects”.

Inkjet contracted -6 percent, but remains the dominant segment with 58 percent share, and 15.1 million devices shipped, with 85 percent of these MFPs. Monochrome grew 3.5 percent, but ranks second in units shipped (8.2 million) and value ($5.4 billion/€4.04 billion), and has a 31 percent share of the market in terms of shipments and a 39 percent share in terms of value.

Colour laser in turn is the “strongest technology growth segment”, with 9.7 percent growth and a 43 percent share of the shipment value market, as well as a seven percent share of shipments. Colour laser also features in 59 percent of MFPs, and as a market alone it saw year-on-year growth of 13 percent, which “beats these same metrics” for monochrome laser, with 47 percent and five percent respectively.

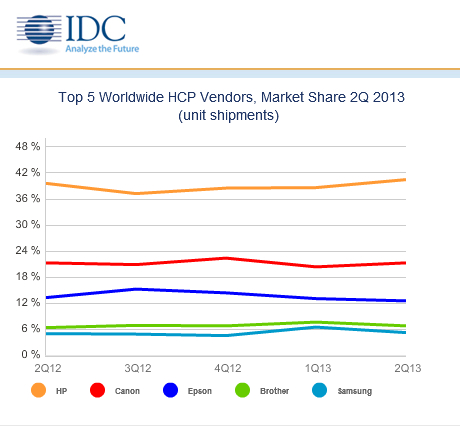

In terms of OEMs, HP remains first with a 40.5 percent market share and an average growth in global markets of five percent, followed by Canon with a -2 percent growth balanced out by a 12.6 percent growth in Western Europe and 2.2 percent growth in the USA, as well as a 14.2 percent growth in the inkjet market in Western Europe. Epson remains in third place, with a decline in shipments of -7.3 percent, only seeing growth in the USA of 12 percent.

Of the other OEMs, Brother and Samsung made up the top five worldwide, with Brother shipping 1.8 million units for a 6.9 percent global share, and a growth of 3.6 percent in unit shipments, whilst Samsung shipped 1.4 million units for a 5.3 percent unit share, and an increase in unit shipments of three percent, thanks to a 28.1 percent growth in Western Europe alone.

Phuong Hang, Programme Manager for Worldwide Quarterly Hardcopy Peripherals Tracker at IDC, stated: “We anticipate that initiatives such as managed print services and wider availability of digitally-based content will continue to gradually shift hardcopy peripheral devices away from the desktop and toward more shared and centralized machines.

“As such, vendors who concentrate on these opportunities should find the best payback for future hardcopy peripheral unit and value shipments.”