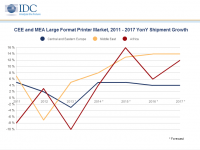

Central and Eastern Europe, the Middle East and Africa (CEMA) region sees a 10.7 percent decline in volume and 5.1 percent year-on-year decrease in value during the first half (H1) of 2013.

Central and Eastern Europe, the Middle East and Africa (CEMA) region sees a 10.7 percent decline in volume and 5.1 percent year-on-year decrease in value during the first half (H1) of 2013.

According to results from IDC, the large format printer (LFP) market in the Central and Eastern Europe, Middle East and Africa (CEMA) region declined during H1 2013, with shipments exceeding 16,300 units valued at $15.36 million (€11.33 million).

Both technical and graphical sub-segments saw shipments decrease in volume terms, although shipments of graphical printing devices increased in value terms, mainly due to strong demand in the Middle East’s construction, advertising and textile industries. The decline in technical LFP shipments, both in volume and value, was attributed to a lack of public tenders, limited construction market investments and prolonged replacement cycles.

As a result of H1 results, IDC expects the overall CEMA LFP market to decline by one percent in 2013, but forecasts a return to growth in 2014.

David Mühlbach, Research Analyst at IDC, said: “The LFP market in the CEMA region is expected to be driven primarily by the Middle East market, where many construction projects have already started and where demand from the advertising printing market is also strong. Central and Eastern Europe is also expected to revive in 2014, due to economic recovery and improved business sentiment. A new EU funding period will also play a supportive role. LFP sales in Africa will increase as well, due to improved political stability and the resumption of postponed projects.”

Aqueous ink-type devices led the market, representing over 80 percent of the market’s volume in the CEMA region this year, and are expected to maintain their dominant market share; while advanced, more environmentally friendly and economical ink types, such as UV and eco-solvent devices, are also expected to gradually increase their market share at the expense of solvent ink.

In terms of vendors, HP remained the overall market leader for the region with a 53.4 percent share of the market in H1 2013, including a 64.3 percent market share in the technical MFP market – the OEM’s traditional stronghold – mainly due to sales of its new DesignJet T-series printers.

In second place was Canon with a market share of 15.2 percent. Shipments of the company’s graphical devices grew significantly, claiming a market share of 11.6 percent in H1 2013. Epson meanwhile ranked third overall with a 15.3 percent market share, and continued to lead the graphic application market with a 35.8 percent share. These positive results were helped by improved availability of the OEM’s SureColor models in 2013.