IDC has reported that the global market grew 4.1 percent in the final quarter of 2013 alone.

The analyst reported that “most regional markets” reported year-on-year growth for the quarter, with a cumulative quarterly growth of 4.1 percent. Shipments increased to 82,000 units in the fourth quarter, an increase of 4,000 on the previous quarterly period, and both “mature and emerging” markets saw growth, with mature markets seeing 3.6 percent growth and emerging markets 4.8 percent growth.

However, despite the strong performance of the global market in the second half of 2013, the whole year showed a decline of 1.7 percent in shipments in terms of wide-format machines. Technical printers saw a third consecutive quarter of growth, with an increase of 6.9 percent and 49,500 units shipped in the quarter and a 4.6 percent increase to 110,800 units for the year. This made it the largest application segment with a 60 percent share, up from 59 percent in 2012.

Graphics application shipments meanwhile were flat compared to 2012, with 32,500 units shipped, giving it a 40 percent share of the total market, down one percent from a year ago. Emerging markets saw a 4.8 percent growth whilst mature markets saw a 3.2 percent decline.

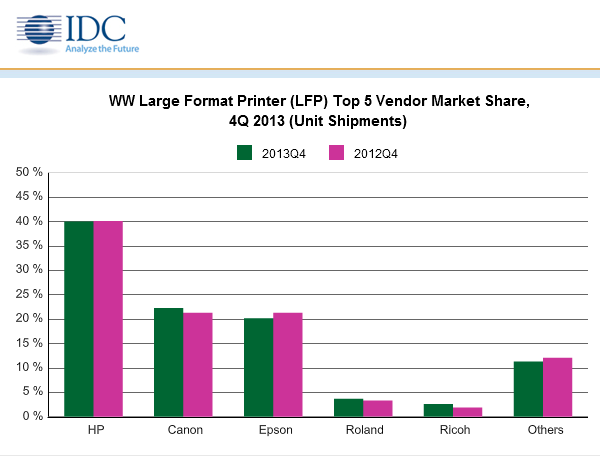

In terms of the OEMs and their market shares, HP grew by 3.9 percent to over 32,801 units shipped – a 40 percent market share “essentially unchanged” from 2012, meaning it remains the market leader in the technical sector with “more than double the share” of Canon in second place. HP also remained in second place in the graphical sector behind Epson.

Canon climbed to second place in the total global market with 22.3 percent of the market, a growth of 8.5 percent over 2012 and 18,247 units shipped, as well as seeing growth in technical and graphics, whilst its yearly growth was 7.5 percent. Epson placed third with 20.2 percent of the market, one percent down from 2012, with a 1.1 percent decline in shipments to 16,577 units, and it was third in the technical market but remains leader of graphics, with a yearly total decline of 4.5 percent in the global market.

In fourth place was Roland, with a quarterly growth of 17.2 percent, giving it a 3.7 percent market share with 3,009 units shipped. The OEM’s strength is said to be the graphics market, in which it holds fourth place, and it posted a year-on-year increase of 13.6 percent. Finally, Ricoh came fifth with a 2.6 percent share of the market, significant quarterly growth of 41.8 percent and 2,126 units shipped, with technical its only market, and its yearly growth reached 24.2 percent.

Phuong Hang, Programme Director for IDC’s Worldwide Large Format Printer Tracker, stated: “There are multiple growth opportunities in this market. For instance, improved speeds and image quality can boost aqueous sales into the technical space. Latex ink-based products will be a growth driver as well. Vendors are touting lower power consumption of this technology, and the ability to print white ink accesses applications that use transparent media.”