An article has looked at “the big picture” for the office supplies sector in the region.

An article has looked at “the big picture” for the office supplies sector in the region.

The blog by Ian Elliot, from E&S Solutions, comes after a “mini-marathon series of blogs that attempted to provide a detailed overview of the workings of the office supplies component of the office products industry”. Elliot noted that the market is a “big, complex industry”, adding that “there’s nothing simple about a $25 billion (€23.1 billion) ink and toner market that keeps 12 OEMs, with combined global sales of $170 billion (€157 billion), afloat!”

He noted that his purpose in the series and in the summary piece was to “provide information that may help smaller, independent resellers to develop a better understanding of the market, which may, in turn, help them plot a strategy to improve their business prospects”. He also produced an infographic to better explain and “simplify the complexity into a visual with a few key points”, with the infographic featuring five distinct sections.

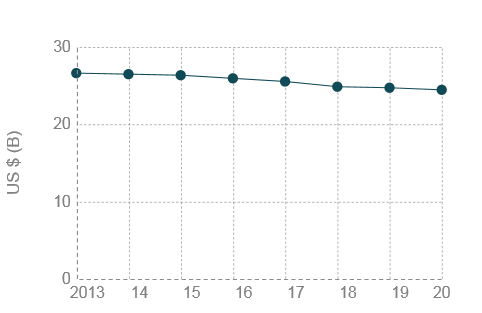

The first points out that the market for ink and toner in the USA, “although modestly declining, remains very large” at around $25 billion “as measured in retail dollars”, with an annual decline of around 1.5 percent a year, though the “biggest decline” is monochrome toner, which is falling by four percent a year, and where the aftermarket has “the largest share” of 30 percent.

He expands on this in his second point, noting that the aftermarket is “facing a disproportionate loss in share because the market for monochrome products” is falling, while the market for colour “where it has less than 10 percent share” is “still increasing slightly” at around one percent a year. Additionally, “despite the maturity of the market the OEM still has a dominant share”, with the aftermarket facing a loss of $500 million (€463 million) in retail dollars by 2020, and of market share to 15 percent.

His third point discusses “pricing by product and by channel”, noting that “the only reseller channel that can make any money selling office products and supplies” are tier two and three independents, and “only then, if they focus on OEM conversions targeting accounts” that tier one resellers “currently have a stranglehold over”.

OEMs have “pricing power”, and “have maintained (even increased) prices”, with a usual price spread of 20 to 25 points between OEM and tier one aftermarket products sold through tier one distribution, while tier two aftermarket sales “are typically” discounted 25 percent compared to tier one, but Amazon offers even a third less than this.

His expanded point here is that “typical” tier two and three resellers “have little to no online authority”, as well as “poor websites, weak information technology assets, and little to no engagement with a social audience”, with tier one resellers of OEM products and tier one aftermarket products not making any money. In turn, tier two resellers of tier two aftermarket products “make money once they exceed” around $500,000 (€463,050) in annual sales.

Based on the Amazon model, “no one’s making any money – it’s only sustainable while Amazon ‘buys’ market share”, and Elliot concludes by noting that “in a nutshell, it’s a big market that offers a significant revenue and profit growth opportunity. But, the only way to participate, is to enter the digital world and focus on the ‘blue ocean’ customers currently purchasing high-priced cartridges through the Tier-1 resellers”.